HOW MUCH LIFE INSURANCE DO YOU NEED?

If you calculate the amount of insurance a person really needs, you would find that most people are really underinsured. The only way that most of us can be adequately insured is to invest in a Term Life Insurance policy. Group Term Life Insurance would be even CHEAPER. (Ask me, I should know better!)

The general rule for life insurance coverage is to be insured 10 times your annual income.

If you compromise by reducing the coverage to maintain a lower premium, that is bad for you or your beneficiary and beats the purpose of taking insurance in the first place. If you maintain the high coverage, you end up paying through your nose!

The most comprehensive method to determine the amount of insurance you need is by using the ‘needs approach’. All upcoming expenditures are reviewed to determine the amount of insurance needed. Total assets and other incomes are subtracted from the total financial obligations to determine the amount of life insurance needed. These obligations include mortgage payments, future education expenses for children, future income for family, funeral expenses etc.

Your insurance salesman will ask you to

i. buy a permanent life insurance (insured up to age 100)

ii. increase your life insurance coverage.

iii. increase your critical illness coverage

iv. increase your personal accident coverage to include hospital income

v. increase your lifetime limit for your medical card

vi. extend your medical coverage up to age 100

HOW TO SOLVE YOUR INSURANCE NEEDS?

Prudential’s PRUhealth policy which is sold as a rider to its investment-linked insurance plans provides comprehensive coverage up to age 100. A 70-year-old client who buys the PRUhealth plan will pay about RM480 a month as premium (for cover expiring at age 80), or RM611 for cover expiring at the age 100 based on the lowest plan PRUhealth100. For those aged between 26 and 30, the premium for the plan with cover expiring at age 80 starts from RM94 a month. (The Star,5 th September 2010)

By 2050, the average lifespan is expected to increase to 77 years for men and 82 years for women. Insurance companies now provide medical plans that cover the policyholders up to age 100. Do you really need to extend your medical coverage up to age 100 when your life expectancy is 80? Do you know the insurance charges?

When buying insurance, the main concern is the coverage. Of course, the higher the coverage the better it is. If the policy covers you until age 100, so much the better. The price you have to pay for the high coverage as well as the terms and period of coverage will be very high. If you compromise by reducing the coverage to maintain a lower premium, that is bad for you or your beneficiary and beats the purpose of taking insurance in the first place. If you maintain the high coverage, you end up paying through your nose!

The solution to solve your insurance needs is to take calculated risk and to plan to become SELF-INSURED eventually. Contact me and I will show you how! For the same amount of coverage, you pay much less for term life insurance as compared to whole-life insurance. The LESS you spend on insurance, the MORE you save. The more you save, the more you can invest. The end result is you can retire comfortably.

A BETTER PLAN

Buy TERM INSURANCE and invest the difference in premium. Better still, invest RM200 or RM300 every month in a mutual fund. Thirty or forty years later, when the kids are grown-up, the house is paid for, and you have more than RM700,000 in mutual funds, you’ll become self-insured. That means when your 30-year term insurance is up, you shouldn’t need life insurance at all – because with no kids to feed, no mortgage payment, and over RM700,000 investment value in mutual fund, you become self-insured. If you die, your spouse will inherit the investment value which is much much more than the death benefit from your insurance policy.

TYPES OF LIFE INSURANCE

Term life insurance provides maximum coverage for the least cost. It is the CHEAPEST form of life insurance if you do not know how to get Group Term Life Insurance.

The insurance salesman will convince the client to buy a whole life policy because unlike term life, it provides coverage up to age 100. Moreover, you will get back your money(based on the cash value) when you surrender your policy later on. You can also borrow against your cash value if you need money urgently. Of course you have to pay interest on the loan taken. It is a form of forced savings for your retirement

Investment-linked insurance is very flexible. You can vary the sum assured of the basic policy and riders. You can add or remove riders and utilize premium holidays and partial withdrawal options without incurring any interest charges. You may also switch funds or change your premium and investments anytime.

Investment linked insurance provide coverage up to age 100. The insurance charges will be deducted through the cancellation of units from the unit funds. Your investment linked insurance will be terminated if there are insufficient units to pay for the fees and the high insurance charges especially when the charges are increased over time.

Because of the higher premiums of whole life and endowment policies, term life is the only viable type of policy – one that can provide a large enough coverage at a reasonable cost. Stick with coverage when it comes to insurance. Insurance is about protection. As for returns, invest your hard earned money in other more appropriate financial products such as unit trusts which can give you higher returns. It is not worthwhile to use insurance as a savings plan. Any form of insurance that involves you getting money back somewhere along the line would mean that you are using it as an investment vehicle and not for protection.

Rule of 72

The rule of 72 is this: take the interest rate you earn on money and divide that number into 72. The answer tells you how many years it takes to double your money. Assuming I could earn 12% annual interest, I take the number 72 and divide it by 12. The answer is 6. Therefore at 12% annual interest, it takes 6 years for RM1,000 to double in value to RM2,000. In another 6 years, RM2,000 would again double and be worth RM4,000.

If you gave me RM1,000 and I gave it back to you in 12 years time, you will only be getting ¼ of the money you gave me. You would be getting RM250 of your original money and RM750 in interest. The other RM3,000 is in my pocket. So don’t be too happy when the insurance salesman tells you that after 18 years, you will get back all the money you have paid.

Shop for your Insurance Needs

The sad fact is most people do not buy life insurance. They are sold life insurance. People will shop all over to get the best deal for whatever they are buying but when it comes to buying life insurance, they will buy whatever the salesman is recommending. So get someone like me to shop for your insurance needs. I can even show you how to buy group term life insurance. Insurance salesmen claim to provide financial planning services. I provide unbiased financial planning services

Guidelines on Product Transparency and Disclosure

The recent Guidelines on Product Transparency and Disclosure will improve consumers’ understanding of key product features, their risks and benefits and major terms and conditions. Policyholders will be more aware that returns are NOT guaranteed. The Product Disclosure Sheet also outlines the fees, commission and the insurance charges and hence will serve to facilitate comparative shopping by potential customers. When it is disclosed which portion of the premium goes towards providing coverage, you will be able to do a cost benefit analysis of the policies and check whether you are paying a fair price for coverage.

WILL YOU REALLY NEED THAT MUCH TO RETIRE?

So how much would one need for retirement? Experts say this depends on the individual and his lifestyle and how much he is willing to reduce consumption – to eat out less often, buy fewer things, drive less, drive a smaller car and travel less. The rule of the thumb is managing on 60% of your last drawn pay. Some critics suggest that using the 60-per-cent number is a scare tactic on the part of the financial industry to panic people into saving more than they need to, enriching the industry in the process. Many middle-income group are so fixated on saving earlier in life that they are unnecessarily depriving themselves of enjoyment.

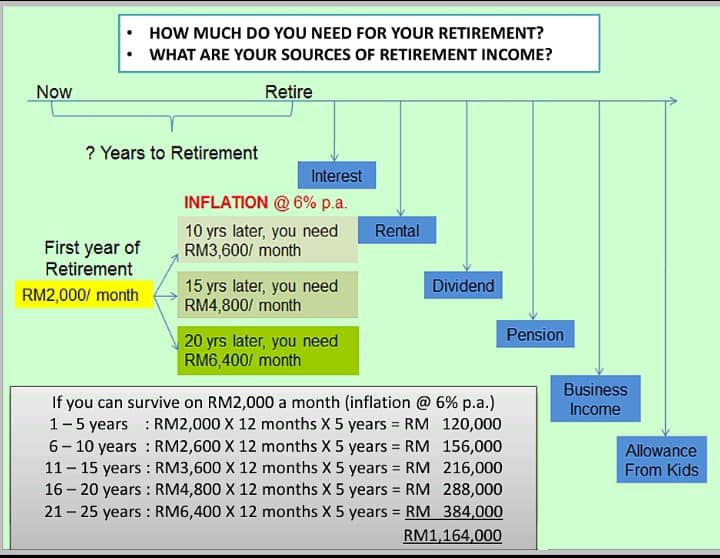

HOW MUCH DO YOU NEED FOR YOUR RETIREMENT?

In investing, you should not be looking at the date of retirement but rather the date of potential death which is probably still another 25 years away after retirement. The risk with fixed deposits is the interest rate can’t meet the inflation rate and the purchasing power of money is getting smaller. Given the current life span, it would do retirees good to take calculated risk in their investment.

It is not how much you earn but how much you INVEST that determines your retirement fund.

If EPF savings is NOT taken into account, inflation is NOT calculated throughout retirement years and living expenses just include food, clothing, transport, utility bills, home entertainment and medication:

Scenario : If you retire now and you can survive on RM 2,000 a month (inflation at 6% p.a)

| 1-5 yrs : RM 2,000 X 12 mths X 5 yrs = | RM 120,000 |

| 6-10 yrs : RM 2,600 X 12 mths X 5 yrs = | RM 156,000 |

| 11-15 yrs : RM 3,600 X 12 mths X 5 yrs = | RM 216,000 |

| 16-20 yrs : RM 4,800 X 12 mths X 5 yrs = | RM 288,000 |

| 21-25 yrs : RM 6,400 X 12 mths X 5 yrs = | RM 384,000 |

| Total = | RM 1,164,000 |